July 24th—Un and Underserved People’s Identity approach receives IDESG Privacy Committee Review approval. This means that wider adoption of such an approach is more feasible.

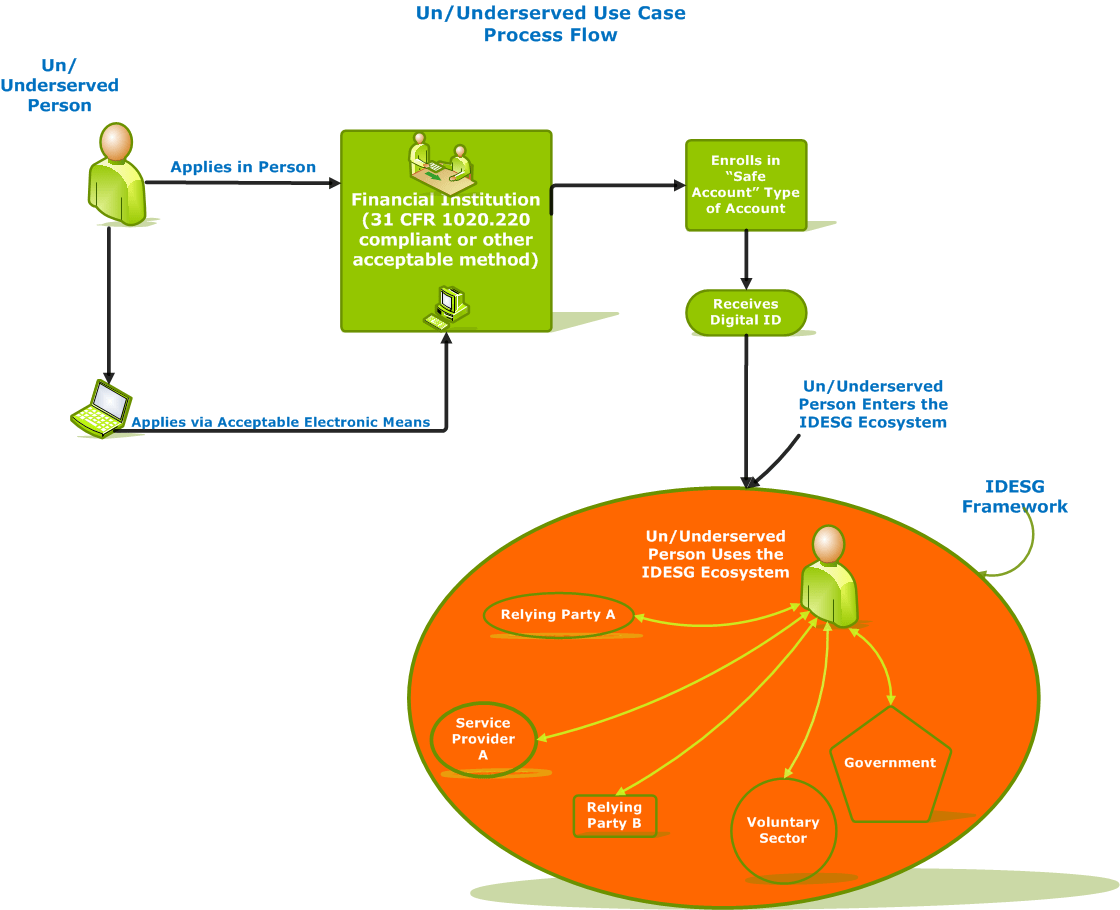

Un and Underserved Use Case Process Flow

One of the indices of the human trust experience is whether or not and the extent to which a person or organization creates work that serves others and interests separate and greater than themselves. My view is that particularly today economic development should wherever possible be designed to serve the under served first. To this end I have worked on a systemic approach (at the IDESG referred to as a “Use Case” for identity management and privacy for the Un and Underserved People for the Identity Ecosystem Steering Group (IDESG). In essence this approach allows individuals who have been left out of the existing online environment to piggy back into interactions and transactions online through identities received through Federally Insured bank accounts. This can be done remotely as well as in person. There are many advantages to this approach which will be reported on in the coming months. The good news is that on July 24th this approach received IDESG Privacy Committee Review approval. This means that wider adoption of such an approach is more feasible.

For complete information see https://www.idecosystem.org/wiki/Un_and_Underserved_People_Use_Case

Use Case Description

“Use Case Purpose”: Un and Underserved People Enter the IDESG Identity Ecosystem.

Un and Underserved refers to people that do not have, have lost, or have inadequate digital identities to enable them to participate in the secure and resilient, cost effective and easy to use, privacy enhancing and voluntary interoperable online Identity Ecosystem envisioned by NSTIC and the IDESG. Currently there are barriers to and opportunities for the Un and Underserved to enter the IDESG Identity Ecosystem. Such barriers may be, limited financial means, physical disadvantage or challenge, language differences, loss of employment, to name but a few. Such opportunities may be new products and services to remove these barriers, innovations in serving this community as well as greater social cohesion and internet-wide cyber-security. Importantly, many of the Un and Underserved are also financially un and underserved. Today 68 million American adults are un or under banked. More than 2.5 billion adults around the world are unbanked.

The goal of this use case is to leverage existing programs and services, for example the FDIC “Safe Account” program, to allow the Un and Underserved to use their “Safe Account” bank account enrollment process as a means of obtaining a digital identity and entering the IDESG Identity Ecosystem. Being Un and Underserved is not a new problem but one that has had a long (perhaps going back to the beginnings of money and then banking)and often intractable set of complexities. The efficiencies of cyberspace (the internet) provides an historic opportunity to bridge this gap.

Scenario(Example): Julia, a prospective underserved financial services customer, wants to open a bank account as well as obtain an digital identity for use in the IDESG Identity Ecosystem. Julia learns of a FDIC “Safe Account” type of account at her local community center which allows her to apply for an account and subsequently obtain a digital identity. Julia applies for and gets an FDIC “Safe Account” through an FDIC insured bank or equivalent financial institution compliant with 31 CFR 1020.220 – Customer identification programs (CIP) for banks, savings associations, credit unions, and certain non-Federally regulated banks. Or other acceptable customer identification program. The enrollment vetting process into a “Safe Account” serves the vetting requirements for Julia to obtain her digital identity. After a period of successful Safe Account practices Julia uses her Safe Account history and digital identity to apply for an FCCX credential or other governmental credential for accessing government services. Julia receives the government credential and uses the government credential to apply for other online services and products including more financial services. Julia is able to step by step build access to a wide range of products and services she will need and use as she provides for her family and builds her entrepreneurial life as a clothes designer and pattern maker.

Goals Summary: Julia will be able to obtain an digital credential with the qualifications used to obtain her Safe Account. Julia will be able manage her finances in a secure and insured or protected environment where she can increase her income through entrepreneurship, improving the quality of life for herself and her son, the economic activity in her neighborhood through her purchases, and tax receipts to her city and state. Julia will be able to interact with some government and non-profit services improving confidence in government and non-profit institutions and financial institutions including banking. The financial institutions and non-profit organizations, government agencies and healthcare providers will be able to increase the number of their customers/participants. Through this use case a broad range of stakeholders are brought together to share risks and rewards in creating an online Identity Ecosystem Framework where economic opportunity, productivity and human well being are harmonized.

Actors:

- 1 Un and Underserved People.

- 2 Financial Institutions.

- 3 Non-profit Organizations.

- 4 Government.

- 5 Insurance entities.

- 6 Any Relying Party or Service Provider in the IDESG Identity Ecosystem that complies with the NSTIC principles and has a Trustmark Accreditation.

- 7 Alternative Financial Services.

Assumptions Un and Underserved Person applies in person at the Financial Institution or uses an acceptable electronic means of application including for example Treasury’s OCIP that has brought together the FSSCC, DHS, and NIST to create a Cooperative Research and Development Agreement on identity proofing, which has identified new methods for satisfying the “know your customer” requirements of financial institutions. Financial Institution must be a FDIC insured bank or equivalent. The digital identity meets the needs of relying parties.

Process Flow

This use case is unique in that the person, Julia and her son in this case, exist outside an online Identity Ecosystem. Entering the Identity Ecosystem is a kind of state change, so to speak, for Julia. The other stakeholders are already inside the Identity Ecosystem. The process of entering the ecosystem should be done with care by all stakeholders. Success Scenario Julia is able to enroll in a Safe Account that provides her with a digital identity useful in the ID Ecosystem for products and services and for federal, state and local governments. Julia can also apply for and potentially receive other digital identities from other ID Ecosystem providers enlarging the range of products and online services, including financial she can access.